Profit and loss account of credit institutions as at 31 March 2017

Press release 17/21

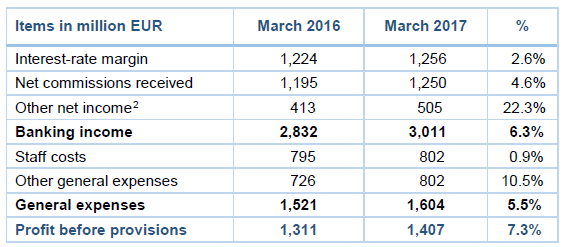

The CSSF estimates profit before provisions of the Luxembourg banking sector at EUR 1,407 million for the first three months of 2017. Compared to the same period in 2016, profit before provisions thus increased by 7.3%.1

The positive development of the profit before provisions of credit institutions in Luxembourg results from the substantial rise in the banking income (+6.3%) which allowed offsetting the continuing escalation in general costs. This positive aggregated development is, however, divided heterogeneously among credit institutions in Luxembourg. Indeed, on 31 March 2017, 33% of the banks (representing 9% of the banking income) recorded a cost-to-income ratio exceeding 80%.

The increase of the aggregated banking income is due to a favourable development of all its components. The interest-rate margin increased by 2.6% despite the low or even negative interest rates. The interest-rate margin of more than half of the Luxembourg credit institutions developed positively. This favourable development is linked, among others, to two major phenomena: (i) a growth in business volume, and (ii) an impact of negative interest rates by certain banks vis-à-vis their institutional customers.

The increase in net commissions received was observed in over half of the banks in Luxembourg. The rise in these net commissions received, which mainly result from asset management activities on behalf of private and institutional customers, is linked to the very favourable stock market environment year-on-year, which however contributed to investment funds showing highly positive trends during the same period. Other net income recorded a significant increase (+22.3%) as compared to the same period last year. This item is very volatile due to its composition. The rise recorded over the three first months of 2017 as against the same period in 2016 is mainly attributable to non-recurring factors specific to a limited number of banks of the financial centre.

General expenses rose by 5.5% over a year. This increase is linked to the other general expenses (+10.5%), whereas staff costs only rose by 0.9% over a year. This increase in other general expenses concerns most of the banks of the financial centre and reflects the investments in new technical infrastructures, charges due to extraordinary events as well as costs to be borne by banks in order to comply with a wider and more complex regulatory framework.

As a result of the above-mentioned developments, profit before provisions increased by 7.3% year-on-year.

Profit and loss accounts as at 31 March 2017

1 Due to major changes in the banking prudential reporting in 2016, the aggregation scope has been adapted to better reflect the evolution of the profit and loss accounts of Luxembourg banks. Consequently, the figures for March 2016 have been readjusted to reflect a larger aggregation scope which is similar to the new reporting of March 2017.

2 Including dividends received.