Profit and loss account of credit institutions as at 31 March 2018

Press release 18/20

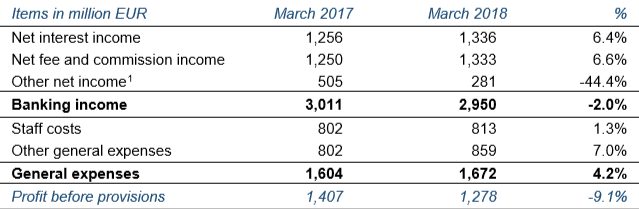

The CSSF estimates profit before provisions of the Luxembourg banking sector at EUR 1,278 million for the first three months of 2018. Compared to the same period in 2017, profit before provisions thus decreased by 9.1%.

The negative development of the profit before provisions of Luxembourg credit institutions during the first three months of 2018 has two main causes: (i) the ongoing increase of general expenses (+4.2%) and (ii) the significant reduction (44.4%) in the other net income. These adverse effects were partially mitigated by the positive result recorded on the main banking activities such as banking intermediation and asset management.

The net interest income registered an increase of 6.4% year-on-year. This trend is shared by half of the banks of the financial centre. The prolonged application of negative interest rates on deposits collected from institutional customers, the rise of the balance sheets and the improved average return on assets are some factors which, depending on the banks, explain the favourable development of the net interest income compared to the previous year.

An increase in net fee and commission income (+6.6%) was observed in half of the banks. The rise in this net fee and commission income, which is largely attributable to the activities related to asset management on behalf of private and institutional customers, is directly linked to the upward trend of financial markets and the very favourable development of the investment fund industry.

As regards other net income, a significant decrease (-44.4%) was recorded as compared to the same period last year. Due to its composition, this item exhibits high volatility and its development is often linked only to non-recurring factors affecting a limited number of banks of the financial sector. For instance, the negative development of exchange differences of some banks, closely related to the development of the EUR/USD exchange rate, was the main reason for the reduction in this item.

General expenses continued to grow (+4.2%) during the first quarter. This growth is primarily related to other general expenses (+7%) and, to a lesser extent, to staff costs (+1.3%). In aggregate terms, general expenses grew faster than banking income thus further reducing the profitability of banks as expressed by the cost-to-income ratio which has risen from 53% to 57% year-on-year.

As a result of the above-mentioned developments, profit before provisions decreased by 9.1% year-on-year.

Profit and loss account as at 31 March 2018

1 Including dividends received.