Revue Thématique des informations relatives au climat publiées par les émetteurs (uniquement en anglais)

Executive summary

Environment, including climate-related matters, is at the forefront of trends affecting companies and capital markets. Indeed, there is a growing recognition that issuers need to consider the importance of these issues, including the potential impacts from the risks and opportunities associated with climate change. In that particular context, the European Union has recently published its updated guidance on non-financial reporting for companies on how to report the impacts of their business on the climate and the impacts of climate change on their business. Such updated guidance is part of the guidance of the key aspects of the Directive 2014/95/EU (the ‘NFI Directive1’).

Thus, the CSSF has carried out a thematic review to examine the current status of climate-related information reported by issuers, by comparing it with the recommendations made in the above-mentioned updated guidance.

We note that, in general, only a small and unsatisfactory percentage of issuers address the questions in relation to climate-change beyond the basic requirements of the NFI Directive. Moreover, while the importance of climate-change effects is relatively well highlighted in the description of business models (for those disclosing climate-related information), we observe a lack of information about concrete actions beyond commitments made or proposals to significantly reduce global warming.

In a more specific way, a notable feature of the new guidance is to provide more insight on the governance aspects, including the board’s oversight of climate-related risks and opportunities and the management’s role in assessing and managing these risks and opportunities along with the information provided on policies and due diligence processes. In the information reviewed, this is a significant omission and there is therefore a clear need for improvement in future non-financial reports as it allows stakeholders to understand the robustness of the company’s approach to climate-related issues.

Consistently with the above, there is a lack of disclosures on risk management in relation to climate-related risks (identification / assessment / mitigation) in the short, medium and long term for a large majority of issuers. There is also a significant need for disclosures in relation to the key climate-related risks, distinguishing physical and transition risks. This absence of disclosures may cast a doubt on the existence of a real action plan, or indicate an underestimated impact of such risks on the operations.

Finally, while issuers already disclose relevant key performance indicators (‘KPIs’) to support some of their climate-related disclosure, the new guidance introduces many new indicators which may be considered in the future. We also recommend issuers willing to achieve a better non-financial reporting to proactively monitor the Taxonomy Regulation developments.

Background

The publication of non-financial information by companies is governed in Europe by Directive 2014/95/EU, as transposed in national legislation, which requires certain large undertakings and groups to provide non-financial and diversity disclosures.

In 2017, the European Commission published its guidelines to help companies to disclose environmental and social information in compliance with the NFI Directive (the ‘Guidelines’).

In June 2017, the Taskforce on Climate-related Financial Disclosures (the ‘TCFD’), initiated by the Financial Stability Board, delivered its recommendations2 on corporate transparency on climate issues. These are organised around four pillars: governance, strategy, risk management, indicators and metrics. The approach has gained international acceptance, although progress is still needed to further implement the recommendations and many challenges remain.

In June 2019, the European Commission published a supplement to its Guidelines on how reporting climate-related information that integrate and complement the existing TCFD recommendations (the ‘Supplement to the Guidelines’).

This Supplement to the Guidelines, that is non-binding like the Guidelines, proposes climate-related disclosures for each of the five reporting areas listed in the NFI Directive: (a) business model, (b) policies and due diligence, (c) outcomes of policies, (d) principal risks and risk management and (e) key performance indicators. This supplement is intended for use by companies that fall under the scope of the NFI Directive and is a recommended tool in view of complying with requirements of the NFI Directive regarding environmental disclosures, particularly with respect to climate change. It may also be useful for other companies that wish to disclose climate-related information.

Purpose, scope and methodology of the thematic review

Considering such recent guidance and the growing expectations of investors and other stakeholders on the quality and comparability of climate-related disclosures, the CSSF has examined the current state of climate-related reporting for a selection of issuers under its supervision.

The objective of this thematic review is not only to assess the compliance of these issuers with the implementation and application of the TCFD’s recommendations and with the Supplement to the Guidelines (all together referred thereafter as the ‘Recommendations’), but also to provide information on the progress to be made in the context of such recommendations.

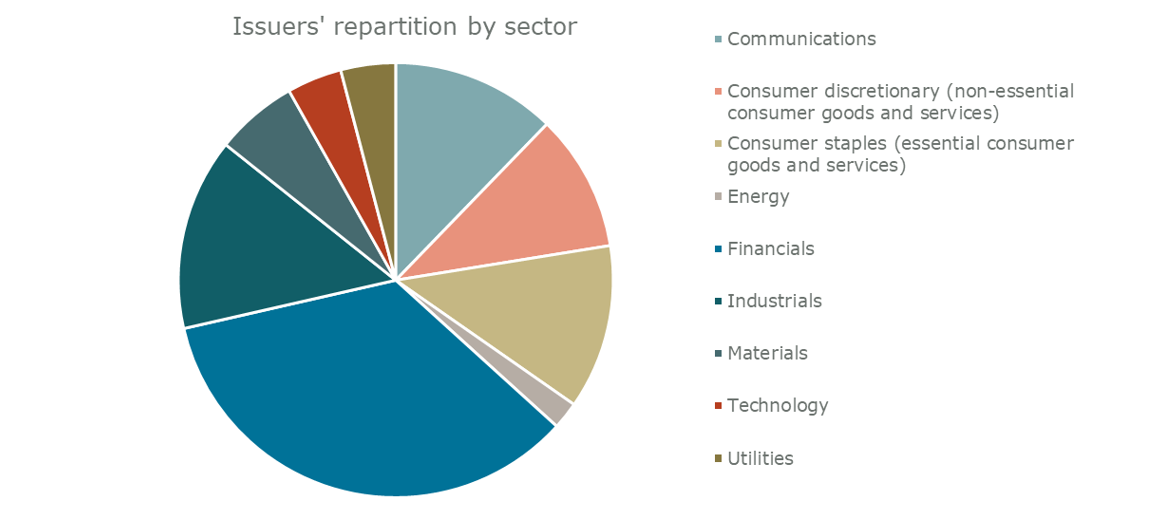

In total, the number of issuers reviewed for this examination is 49. The scope has been determined by including not only issuers subject to the NFI Directive requirements, but also issuers that have voluntarily published non-financial information and for which the publication of information in relation to climate-related matters may be of significant interest to investors and other stakeholders (13 issuers). Based on the Bloomberg Industry Classification Standard, the population of issuers examined is spread across 9 macro-sectors.

The methodology of the examination consisted of a desktop review of the climate-related disclosures included in the 2019 non-financial information of the selected issuers, based on the Recommendations.

This report sets out the key findings of this review, by following the structure of the NFI Directive.

Review of the implementation of the Recommendations by issuers in their non-financial reporting

Overall

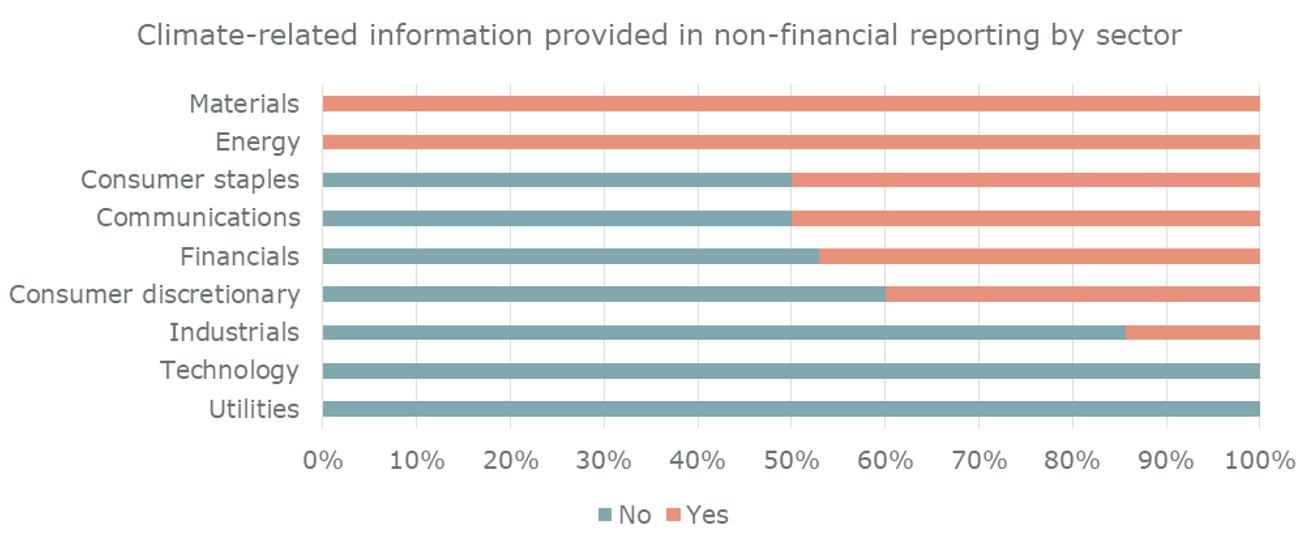

The NFI Directive requests issuers to present information in relation to environmental matters, including non-financial KPIs. The starting point for this examination was then to identify, among the issuers selected, those who provide comprehensive disclosure in relation to climate-related matters. For such purpose it was not considered sufficient for issuers to report only information in relation to their consumption of Greenhouse Gas (‘GHG’), for instance, without any contextualization of the information.

Only 2 out of 5 issuers in our sample provided more or less extensive climate-related information in their non-financial reporting for 2019. As it may be observed in the following table, issuers operating in the sectors (Energy, Materials) that are most directly affected by environmental issues, and more particularly by climate change, all provided climate-related information in 2019. Nevertheless, it is quite surprising that others did not, including issuers operating in Industrials, Technology and Utilities sectors that are also heavily dependent on raw materials, energy, etc.

We recognise that the content of climate-related disclosures may vary between issuers according to various factors (i.e. the sector of activity, geographical location, etc.). It is however expected that issuers consider the double materiality perspective introduced by the Guidelines in the context of reporting climate-related information:

- The financial materiality when reference is made to the development, performance and position of the company, and

- The environmental and social materiality when reference is made to the impact of its activities.

Given the systemic and pervasive effects of climate change, we would expect most companies, within or outside of the scope of the NFI Directive, to be more or less affected by climate change and to provide some level of information in this regard. Therefore, we recommend issuers to provide adequate disclosures and, for those who conclude that climate change is not a material issue, to consider making a statement on this issue, explaining how that conclusion was reached.

The below findings relate only to those 40% of issuers in our sample that have disclosed climate-related information (hereafter referred as the “Reviewed Issuers”).

a. Business model

Business models impact climate change as climate change impacts business models: to move from what was a vicious circle (activities impact climate, climate impact activities) into a more virtuous cycle is quite challenging for most companies. Therefore, issuers are expected to describe how their activities impact climate change, and how climate change impacts their activities.

Recommended disclosures: describe the impact of climate-related risks and opportunities on the organization’s businesses, strategy, and financial planning

Issuers should consider climate-related matters when explaining their business model, in order to allow stakeholders to understand how the climate change impacts their business and their strategy. Overall, nearly all issuers reviewed disclose such information where, in the best instances, climate change is an integral part of their non-financial information, and their objectives are clearly identified in their strategy.

In those cases, the effects of climate change on the issuers’ activities – or issuers’ portfolio in case of real estate assets – are properly assessed and incorporated in business models. A common goal disclosed by many issuers is to reach carbon neutrality: companies consider this corporate citizenship role already as an opportunity itself. This is also often the starting point for revising the business model.

Other opportunities disclosed by issuers include the development of new products, services or processes. There are also opportunities related to resource efficiency and cost savings, or to the adoption of low-emission energy sources. The integration of climate-related risks into the strategy also includes commitments towards sustainability objectives. However, the information currently disclosed is sometimes boilerplate or generic – “using LED lights will save energy and costs!”. The same applies for the identification of climate-related risks and will be further discussed in section d).

Issuers should be more specific, beyond their explanations on the importance of climate change, on the description of climate-related risks on their activities and how the identified opportunities can turn into concrete actions.

Recommended disclosures: describe the ways in which the company’s business model can impact the climate, both positively and negatively

This description has been relatively easy to disclose for the Reviewed Issuers as the causes (the negative effects) and solutions (the positive effects) lie in the same grounds where business models need to be adapted. Thus, examples of information disclosed by Reviewed Issuers are, for entities of the financial sector, the definition of new investment policies for certain products; for entities of the real estate sector, the use of sustainable materials and the construction of energy-efficient buildings; for entities of the transportation and / or logistic sector, the use of cleaner vehicles, etc.

Recommended disclosures: describe the resilience of the organization’s strategy, taking into consideration different climate-related scenarios, including a 2°C or lower scenario

In contrast to the previous recommendations, only two of the Reviewed Issuers, which are leaders in their respective field, have provided a scenario analysis. It is however important, like it is usually done in the field of financial information, to develop different models to assess the resilience of a strategy, especially in adverse cases.

If the preparation of such information may appear more complex, companies may appoint external organizations specialised in the climate field to establish climate scenarios, or use some of the scenarios already available and relevant to them. In addition, it should be noted that a scenario analysis does not necessarily imply changing a set objective, but may simply involve adjusting the timeframe within which the organization would achieve its objective.

In order to provide a relevant analysis, issuers must identify the key stages of their original scenario and its breakdown in the short, medium and long term, as well as the respective consequences when the relevant milestones are not achieved.

b. Policies and due diligence processes

The assessment of climate-related risks and opportunities by companies is becoming common practice in several sectors, especially in the most exposed such as energy and materials. However, even within the same sector of activity, Reviewed Issuers are at different stages of awareness and advancement in terms of assessing climate-related risks and opportunities, putting practices in place and disclosing the methodologies used and the types of risks and opportunities identified. While some firms just started mentioning climate-related risks and opportunities in their non-financial reports, others are actively engaged in producing detailed analysis and internal models.

Thus, disclosing information related to the persons within the organisation and governance structure responsible for setting, implementing and monitoring a specific policy on climate-related matters, permits to inform investors and other stakeholders on the company’s commitment to climate change mitigation and adaptation and the level of its awareness of climate-related risks and opportunities.

In that context, the Supplement to the Guidelines offers specific recommendations regarding the board’s oversight, the role of management and how they assess and manage climate-related risks and opportunities. It notably encourages companies to report on their commitment(s) to tackle climate change.

Recommended disclosures: describe any company policies related to climate, including any climate change mitigation or adaptation policy

With very few exceptions, Reviewed Issuers have unfortunately presented boilerplate or generic information on the involvement of the board and management and on their respective policies on climate-related issues. This makes it hard for stakeholders to evaluate the scope of company’s commitment and ambitions towards climate change.

However, good reporting practices have often in common that they provide in-depth information on how climate-related risks and opportunities have been integrated in the company’s strategy and policies. For example, several issuers have disclosed climate policy that encompasses their activities and operations, indicating a long-standing and ongoing commitment towards achieving climate resilience and providing a dynamic framework for managing their environmental impacts.

To be helpful for investors and other stakeholders, issuers should avoid generic or boilerplate information. Instead, issuers should provide enough details (such as relevant information on how they are committed to climate-related initiatives) for stakeholders to assess their commitment and ambitions.

Recommended disclosures: describe any climate-related targets the company has set as part of its policies, especially any GHG emissions targets, and how company targets relate to national and international targets and to the Paris Agreement3 in particular

Around half of the Reviewed Issuers have mentioned climate-related and energy-related targets they have set as part of their policies and how such targets are consistent with national or international targets.

We recommend issuers to disclose and describe further any climate-related and energy-related targets they have set as part of their policies, and notably explaining the reasoning behind their selection. Indeed, stakeholders are interested in the company’s policies and in any associated targets that demonstrate their commitment to climate mitigation and adaptation, and the related due diligence process.

Recommended disclosures: describe the board’s oversight of climate-related risks and opportunities and management’s role in assessing and managing climate-related risks and opportunities

Once again, based on the information provided, we found that it was generally difficult or not possible to evaluate whether or not climate-related issues receive appropriate board and management attention, to understand well how management is involved in the process of managing sustainability, environmental and climate change risks and opportunities and how these are considered in business decisions. Such disclosures are however useful as they are helping readers to understand the processes and policies used for climate change governance, the issuer’s governance choices, as well as how policies are executed, who is involved and what decisions result from those policies.

For such reason, we recommend that issuers describe in more details the supervision exercised by the board, addressing in particular the following points:

- Processes and frequency by which the board and/or board committees are informed about climate-related issues;

- Whether the board and/or board committees consider climate-rated matters when reviewing and guiding strategy, major plans of action, risk management policies, annual budgets and business plans as well as when setting the company’s objectives, monitoring implementation and performance and overseeing major capital expenditures; and

- How the board and/or board committees monitor and oversee progress against goals and targets to address climate-related issues.

c. Outcomes of climate-related policies

Stakeholders need disclosure of climate-related policy outcomes to help them to monitor and assess a company’s development, position, performance and impact in that context. The Supplement to the Guidelines expresses two Recommendations on qualitative aspects. Quantitative aspects, such as indicators supporting the analyses, are mostly covered in the KPIs section under e) below.

Recommended disclosures: describe the outcomes of the company’s policy on climate change, including its performance against the indicators used and targets set to manage climate related risks and opportunities

Results of our thematic review on these aspects show us that around half of the Reviewed Issuers have described their key climate-related and energy-related targets such as those related to GHG emissions, water usage, energy usage, etc., only in a quantitative manner and do not mention any indication or narrative explanation about achievements related to their targets.

Good disclosure practice on this matter could be, for example, a breakdown of achievements related to a climate-related goal set by the company’s board, with the results receiving a quantified achievement rate.

Thus, we encourage issuers when describing their targets to consider the inclusion of the following:

- Whether the target is absolute or intensity based;

- Timeframes over which the target applies;

- Base year from which progress is measured; and

- Key performance indicators used to assess progress against targets.

Also, where not apparent, issuers may provide a description of the methodologies used to calculate targets and measures.

Recommended disclosures: describe the development of GHG emissions against the targets set and the related risks over time

In line with the observation just made before, we usually found quantitative information about GHG emissions but rarely together with the targets and the related risks over time. Good disclosure practice on this matter could be for example reported information including baseline data, progress information on where the company stands today, allowing for trend analysis.

In order to improve such information, we encourage issuers, when applicable, to provide their Scope 1 GHG emissions (all direct emissions from activities) and Scope 2 GHG emissions (all indirect emissions from the generation of purchased electricity, steam, heat and cooling) and, if appropriate, Scope 3 GHG emissions (all other indirect emissions that occur in the value chain) and the related risks. Also, GHG emissions and associated metrics should be provided for historical periods to allow for trend analysis. Quantitative aspects of such indicators are further discussed in section e).

d. Principal risks and their management

Similarly to the disclosures made on business model, it is important for entities to disclose more precisely the climate-related risks identified. For that purpose, the TCFD has divided those risks in two categories:

- The transition risks, which are the risks of transitioning to a lower-carbon economy and entail extensive policy, legal, technology, and market changes to address mitigation and adaptation requirements related to climate change; and

- The physical risks resulting from climate change, which can be event driven (acute) or longer-term shifts (chronic) in climate pattern.

In respect of the information reviewed, while descriptions of climate-related impacts were present, the identification of specific climate-related risks and their management seem to have been omitted. The Recommendations cover however the following topics:

Recommended topics to be disclosed: the company’s processes for identifying and assessing climate-related risks over the short, medium, and long term, the principal climate-related risks identified, the processes for managing these climate-related risks and how these processes are integrated into the company’s overall risk management.

Clearly these objectives are not met as more than 80 percent of the Reviewed Issuers have not provided relevant information in relation to climate-related risk management.

An unexpected observation is that issuers generally do not disclose how climate-related matters can negatively affect them as it seems that it is difficult for them to see how they harm the environment. An enlightening example is that amongst the entities operating in the agricultural sector, none of them has referred to climate-related risks (droughts, floods, etc.) although they recognise that they have many challenges to face: protect soil and water, recycle waste, etc.

Recommendations require disclosures on risks and strategy to be presented by time frame (which can be defined by the issuer), which must include short, medium- and long-term information on identification and management of climate-related risks. However, only some 20 percent of the Reviewed Issuers provide such explanations. Objectives are rather set over the long term, with regular information on progress made.

Moreover, declaration of intent or commitments made by issuers to long-term goals do not include coercive measures. As issuers could deploy their strategy with few constraints, in particular in the short term, they may omit to disclose a proper risk management policy. As a result, stakeholders are rather confronted with what can be seen as potential attempts of greenwashing than with a well-defined action plan to address climate change challenges.

Issuers are urged to specifically disclose a comprehensive risk management policy in relation to climate-related risks identified in their non-financial reports, in particular the processes for managing those risks and, if applicable, how they make decisions to mitigate, transfer, accept, or control those risks. Information should be given by time frame, i.e. short, medium, and long-term, and definition of such time frame should also be disclosed.

e. Non-financial key performance indicators relevant to the particular business

Finally, quantitative information is needed, as it constitutes the tangible evidence of how an entity really performs.

Recommended disclosures: Disclose the metrics used by the organization to assess climate-related risks and opportunities in line with its strategy and risk management process

KPIs related to GHG emissions

Regardless of how issuers addressed climate-related matters in their non-financial information, GHG emissions are the most recognised KPIs among issuers, even for those that we have considered as not presenting (sufficient) information on climate-related matters (refer to the introductory section). We noted the following:

- Scope 1 GHG emissions are always disclosed and, for 50 percent of cases, entities have presented a breakdown whether by country or region, by business activity or by subsidiary. It is necessary to know how the breakdown is presented in order to understand where efforts shall be directed;

- Scope 2 GHG emissions have only been disclosed by half of the issuers, with an even lower percentage for their breakdown. Scope 2 emissions should not be neglected as they may be a significant lever for companies to lower their emissions, whether by buying “green” electricity, green certificates or by generating renewable energy on-site; and

- Scope 3 GHG emissions have only been disclosed by one third of the issuers. They nevertheless represent reduction cost opportunities, although they are outside the organization’s activity, and foster an engaged dialogue between parties – suppliers or employees – on how to implement sustainability initiatives.

The Recommendations also suggest that, in relation to GHG emissions, entities should indicate the third-party verification/assurance status that applies to each scope, which is barely done by only one fourth of the issuers.

Issuers are requested to give the same emphasis and level of importance to all scope emissions and accordingly, to provide a uniform level of disclosure by scope. Where appropriate, issuers are also requested to present a breakdown to provide stakeholders with a dispersion of their emissions. Like for financial information, verifications or certifications made by third-party represent a significant guarantee for users on how information has been prepared and reported.

Subject to the company’s materiality assessment and in order to facilitate greater comparability of disclosures of non-financial information, the Supplement to the Guidelines invites to consider also disclosing the following other indicators:

KPIs related to energy consumption

In terms of energy consumed, the proposal made is to disclose the total energy consumption and/or the production from renewable and non-renewable sources. This KPI is directly linked to those on GHG emissions, as energy production and consumption account for an important proportion. The majority of issuers has not made such disclosures, or has made it incompletely by only disclosing the total energy consumed. However, this information solely in absolute term is relatively abstract for readers.

The breakdown of energy consumed from (non-) renewable sources is critical to seize the efforts made by a company in this respect, or at least, to identify where progress can be made. When quantitative data are not available, issuers are invited to make this disclosure by type of emission, or by the nature of energy consumed.

KPIs related to assets affected by physical risks

The Recommendations suggest to disclose, in percentage, the assets committed in regions likely to become more exposed to acute or chronic physical climate risks. In line with one of the subjects that need to be improved, i.e. the identification and management of physical (and transition) risks, a direct corollary is the lack of identification of such assets in the non-financial information of the Reviewed issuers. These physical risks assessment and management have been discussed above, and we can only emphasise again the need for their inclusion in the non-financial information as part of a comprehensive long-term climate policy.

KPIs related to Green Financing

The Recommendations suggest to disclose the climate-related Green Bond Ratio (total amount of green bonds outstanding divided by total amount of bonds outstanding) and / or the climate-related Green Debt Ratio (total amount of all green debt instruments outstanding divided by total amount of all debt outstanding). Green bonds finance the companies’ low-carbon transition and are an indicator of how capital is raised for existing and new projects for benefits. This information, when applicable, must be disclosed by issuers.

KPIs related to products and services

Other specific KPIs in relation to climate-related policy are the percentage of turnover, the percentage of investment (CapEx) and/or operating expenditures (OpEx) in the reporting year associated with activities that meet the criteria for substantially contributing to mitigation of or adaptation to climate change as set out in the regulation on the establishment of a framework to facilitate sustainable investment.

We note that these three last listed KPIs are not disclosed by issuers, except for two issuers (same as those mentioned in section a)) which present an information with is compliant with the TCFD Recommendations.

The quantitative information is useful for investors interested to support entities engaging in environmentally sustainable activities. Furthermore, these last disclosure requirements are directly taken from the EU Taxonomy for sustainable activities4 and will apply, in the near future, to entities subject to the NFI Directive. Issuers are requested to proactively monitor the Taxonomy Regulation developments.

Next steps

The results of our thematic review have shown without doubt that there are still significant gaps to fill and that further improvements in the quality and comparability of climate-related disclosures are urgently required to meet the needs of investors and other stakeholders.

Thus, even though the Supplement to the Guidelines – as the Guidelines – remain non-binding, the CSSF urges issuers to review this new guidance which provide practical recommendations on how to better report the impact that their activities have on the climate as well as the impact of climate change on their business. Issuers are expected to exercise their own judgement when deciding which disclosures to use. When deciding whether and to what extent they use the Recommendations, issuers should take account of the principles of good non-financial reporting contained in the Guidelines, including the principles about disclosed information being: material; fair, balanced and understandable; and comprehensive but concise.

We recommend issuers which are not familiar with the TCFD recommendations or with the Supplement to the Guidelines to carefully review these documents and already assess on a voluntary basis their level of compliance with the proposed Recommendations and other guidance. These matters are of an increasing importance and disclosures in that context will be required in the near future, whether by investors, users of information, other stakeholders, and/or regulations.

On 28 October 2020, ESMA released the European common enforcement priorities for 2020 annual financial reports5, in relation to the enforcement of financial and non-financial information. Climate-change is an integral part of these priorities, in particular the disclosure of physical and transition risks as well as any measures put in place to prevent such risks from materialising and to mitigate their effects.

In 2021, the CSSF will carry out a follow up of this examination and of the European priorities in order to continue providing issuers with recommendations and good practices.

More information on examinations by the CSSF within the framework of its mission under Article 22 (1) of the Transparency Law is available on the CSSF’s website (Topics > Enforcement of financial information).