Situation globale des organismes de placement collectif à la fin du mois de mars 2022 (uniquement en anglais)

Communiqué de presse 22/09

I. Overall situation

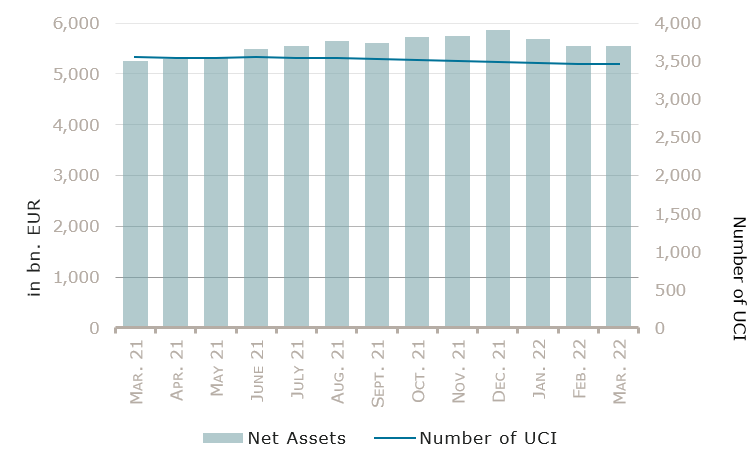

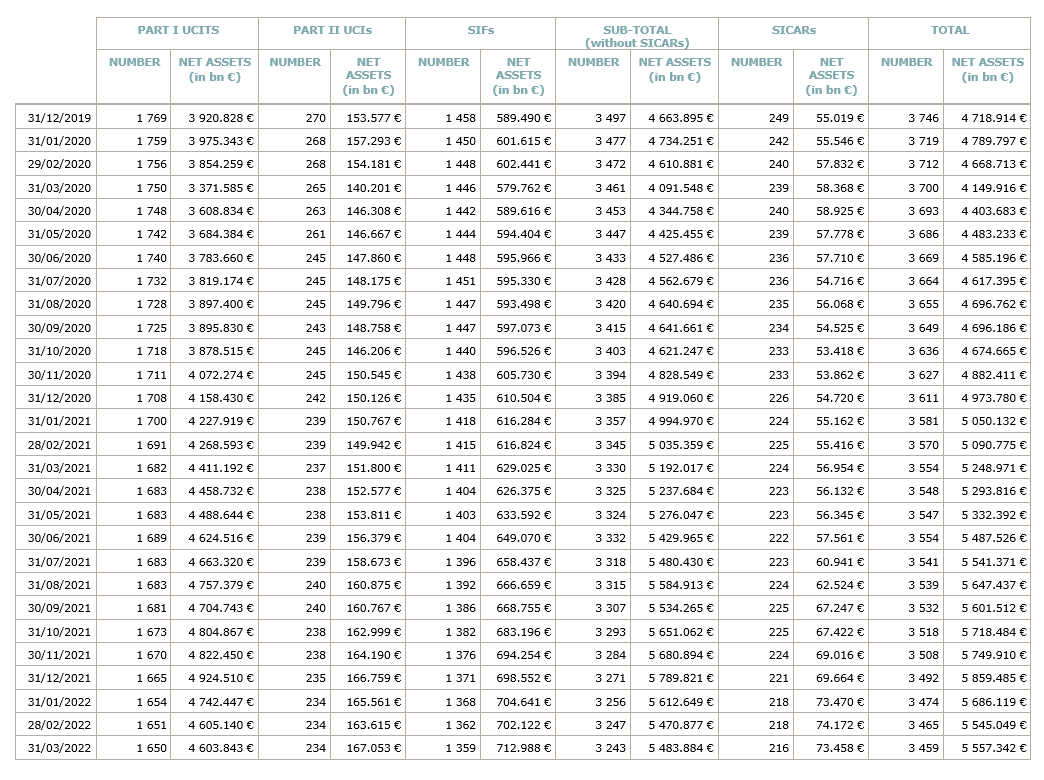

As at 31 March 2022, the total net assets of undertakings for collective investment, comprising UCIs subject to the 2010 Law, specialised investment funds and SICARs, amounted to EUR 5,557.342 billion compared to EUR 5,545.049 billion as at 28 February 2022, i.e. an increase of 0.22% over one month. Over the last twelve months, the volume of net assets rose by 5.87%.

The Luxembourg UCI industry thus registered a positive variation amounting to EUR 12.293 billion in March. This increase represents the sum of negative net capital investments of EUR 14.871 billion (-0.27%) and of the positive development of financial markets amounting to EUR 27.164 billion (0.49%).

The development of undertakings for collective investment is as follows:

The number of undertakings for collective investment (UCIs) taken into consideration totalled 3,459, against 3,465 the previous month. A total of 2,266 entities adopted an umbrella structure representing 13,234 sub-funds. Adding the 1,193 entities with a traditional UCI structure to that figure, a total of 14,427 fund units were active in the financial centre.

As regards the impact of financial markets on the main categories of undertakings for collective investment and the net capital investment in these UCIs, the following can be said for the month of March.

Despite the development of the Ukraine crisis, the volatility of commodity markets, the persistence of inflation concerns and the increasingly stricter monetary policy stances, the UCI equity categories of developed markets recovered and recorded a positive performance, while bond yields continued to rise.

Concerning developed markets, the European equity UCI category registered a positive performance, the PMI business survey exceeding expectations and the geopolitical risks being partly priced out despite Europe recording a deceleration in activity, a dropdown in consumer confidence and high inflation. The US equity UCI category rose in March amid an overall stable US global economic picture with well oriented economic indicators, US labour market and growth continuing to look robust while inflation anticipations remain elevated. The appreciation of the USD against the EUR strengthened the gains. Japanese equity markets followed the upward market trend but, due to the sharp depreciation of more than 4% of the YEN against the EUR, the Japanese equity UCI category finished the month in negative territory.

As for emerging countries, the Asian equity UCI category realised a negative performance, mainly driven by Chinese equity markets on grounds of new lockdowns due to the pandemic in some major cities, the slowdown in the property market and regulatory actions in some sectors. The Eastern European equity UCI category overall declined given the continuation of the Ukraine conflict and the effects of related sanctions, although some equity markets in Eastern Europe such as Poland and Czech Republic registered a recovery. The Latin American equity UCI continued to enjoy strong gains supported by higher commodity prices and the strengthening of domestic currencies.

In March, the equity UCI categories registered a negative net capital investment, mainly driven by outflows in the European equity UCI category.

Development of equity UCIs during the month of March 2022*

|

Market variation in % |

Net issues in % |

|

| Global market equities |

2.57% |

0.28% |

| European equities |

0.82% |

-2.49% |

| US equities |

3.47% |

0.96% |

| Japanese equities |

-0.39% |

-1.31% |

| Eastern European equities |

-4.46% |

5.27% |

| Asian equities |

-4.95% |

-1.14% |

| Latin American equities |

13.32% |

1.79% |

| Other equities |

-0.52% |

-1.26% |

* Variation in % of Nssets in EUR as compared to the previous month

In March, following the persistent inflation figures and the increasingly restrictive monetary policy stances of major central banks, we could observe a rise in bond yields on both sides of the Atlantic.

Concerning the EUR denominated bond UCI category, the European Central Bank (ECB) announced that it expects to conclude its “Asset Purchase Program” (“APP”) by June 2022 and that it could raise interest rates in the second half of 2022, compared to 2023 in its previous communications. Against this backdrop, yields rose (i.e. bond prices fell) and overall, the EUR denominated bond UCI category realised a negative performance.

Concerning the USD denominated bond UCI category, the Federal Reserve (Fed) raised its rates by 0.25 percentage points to 0.5%, further indicating that other rate hikes could follow in order to restore price stability. As a result, the yield curve flattened and even partially inverted on longer maturities. Historically an inverted yield curve over a number of months is used as an indicator of potential recession. Investment grade bond spreads widened during the month and overall the USD denominated bond UCI category decreased.

The Emerging Market bond UCI category finished the month in negative territory as Emerging Markets bonds declined in March in consequence of rising rates, rising inflation, continued struggles with the Omicron variant in China and geopolitical concerns.

In March, fixed income UCI categories registered an overall negative net capital investment. The Global market bonds category experienced the most significant outflows.

Development of fixed income UCIs during the month of March 2022*

|

Market variation in % |

Net issues in % |

|

| EUR money market |

-0.09% |

0.31% |

| USD money market |

0.64% |

-3.76% |

| Global money market |

-0.42% |

1.19% |

| EUR-denominated bonds |

-1.28% |

-0.06% |

| USD-denominated bonds |

-1.50% |

5.07% |

| Global market bonds |

-1.07% |

-1.45% |

| Emerging market bonds |

-0.64% |

-0.77% |

| High Yield bonds |

-0.16% |

-1.88% |

| Others |

-0.82% |

0.41% |

* Variation in % of Net Assets in EUR as compared to the previous month

The development of net assets of diversified Luxembourg UCIs and funds of funds is illustrated in the table below:

Development of diversified UCIs and funds of funds during the month of March*

|

Market variation in % |

Net issues in % |

|

| Diversified UCIs |

0.68% |

0.48% |

| Funds of funds |

1.00% |

0.29% |

* Variation in % of Net Assets in EUR as compared to the previous month

II. Breakdown of the number and net assets of UCIs

During the month under review, the following five undertakings for collective investment have been registered on the official list:

UCITS Part I 2010 Law:

- ALQUANT BEYOND INNOVATION, 4, rue Thomas Edison, L-1445 Luxembourg-Strassen

- GREEN VISION FUND, 1C, rue Gabriel Lippmann, L-5365 Munsbach

- I-AM GLOBAL MACRO CONVEXITY FUND, 9A, rue Gabriel Lippmann, L-5365 Munsbach

- UFT, 1C, rue Gabriel Lippmann, L-5365 Munsbach

- UMWELTSPEKTRUM, 4, rue Thomas Edison, L-1445 Luxembourg-Strassen

The following eleven undertakings for collective investment have been deregistered from the official list during the month under review:

UCITS Part I 2010 Law:

- CANDRIAM QUANT, 5, allée Scheffer, L-2520 Luxembourg

- DEKA-CONVERGENCERENTEN, 6, rue Lou Hemmer, L-1748 Luxembourg-Findel

- DEKA-GLOBAL CONVERGENCERENTEN, 6, rue Lou Hemmer, L-1748 Luxembourg-Findel

- IRON TRUST, 4, rue Thomas Edison, L-1445 Strassen

- MELUSINA INVESTMENTS, 49, avenue J-F Kennedy, L-1855 Luxembourg

- UNIINSTITUTIONAL FINANCIAL BONDS 2022, 3, Heienhaff, L-1736 Senningerberg

SIFs:

- ARISTA S.A. SICAV-SIF, 15, boulevard Friedrich Wilhelm Raiffeisen, L-2411 Luxembourg

- GEODETICA S.C.A. SICAV-SIF, 11-13, boulevard de la Foire, L-1528 Luxembourg

- INOVALIS REAL ESTATE S.C.A., SICAV-SIF, 12, rue Eugène Ruppert, L-2453 Luxembourg

SICARs:

- FIVE ARROWS SECONDARY OPPORTUNITIES III CO-INVESTMENT S.C.A., SICAR, 33, rue Sainte Zithe, L-2763 Luxembourg

- SECOYA PRIVATE EQUITY INVESTMENTS SCA-SICAR, 50, avenue J-F Kennedy, L-2951 Luxembourg